The previous edition as at 1st June 2015 can be found in the archives Click HERE The index is low on the right of the archive blog page.

Ongoing re-writes, updates and additional material are noted on the LATEST UPDATES page.

FOR THE REPAYMENT OF DEBT

L = the debt / loan / mortgage value

If P = 7 p.a. and L = 100, then:

Let's place r% on the same axis so that if an 'X' is placed at r% the position of the 'X' represents a standing loan.

e% p.a. = the percentage rate at which debt servicing payments 'P' p.a. will increase every year.

If ‘e’ is negative the payments are falling.

Example: if P = 100 and e% = 3% p.a. in the following year the new value of P = 103, in any currency.

For the LP (Level Payments) loan, the position of the ‘X’ indicates that e% p.a. = 0% p.a. This is an LP (Level Payments) loan as long as the ‘X’ stays on the vertical, Y-axis, meaning that e% = 0% every year. Level Payments loans are one dimensional - the 'X' stays on the vertical line. Other regular repayment loans in general, like the ones we want to look at are two dimensional - the 'X' moves around an area with two axes.

We will want the 'X' to be to the left of that AEG% line showing the repayments are rising less quickly than average borrowers' earnings, or AEG, are rising. Whether or not AEG is the right or the best index to use will be discussed later.

As just mentioned, the exact definition of AEG% p.a. is something that needs careful thought. But as long as the 'X' is far enough to the left of the AEG% line, as long as the difference between e% and AEG% p.a. is large enough the great majority of borrowers will have earnings which are rising faster than the payments 'P p.a.' are rising. AEG% p.a. is the rate at which National Average Earnings, NAE, are rising.

Of course, most payments are made monthly. Readers should divide the annual figure by twelve to get the monthly payment.

At 4% p.a. payments depreciation, at the end of the first 3 three years the monthly cost would be almost 12% less than NAE.

The position of the 'X' describes the current value of P% and of e%. And the position of the 'X' has a visible horizontal distance from the AEG% p.a. line and a visible vertical distance from the standing loan line - two safety margins to be aware of. Later, these distances will be given names and included in the risk management equation.

USING THE CHART

This means that the ratio P/L never changes and so the value of P% p.a. never changes. It stands still. Normally P% p.a. rises every year as the loan gets repaid. This is because as 'L' reduces as the result of the payments 'P', the ratio P/L rises.

It is like a race in which the payments increases are chasing the loan size 'L' increases. If both are rising at the same rate neither side wins. It is a dead heat.

THE CASE WHEN e% IS NEGATIVE

In maths there is usually a case when variables go negative. It is the same on the charts. What happens to the standing loan line and to the 'X' if the loan is still to be repaid?

Let us place AEG% p.a. on the Y-Axis. AEG% p.a. is not rising. If trouble is to be avoided, both the Loan Size 'L' and the Payments 'P' must be falling. If payments depreciation is say, 4% p.a. and AEG% p.a. = 0%, this means that e% p.a. = -4% p.a.

In this case we have to extend the standing loan line to the left of the Y-Axis:

The 'X' is above the standing loan line but to the left of the Y-Axis. The mortgage is being repaid even though the payments are falling every year. In this particular illustration, the level of payments 'P' is not very high because of the very low nominal rate of interest of 3%. That is what happens when inflation and AEG% p.a. are very low. A low interest rate moves the standing loan line down.

Here is a spreadsheet illustrating how that might work. In the table and on the chart above, AEG% = 0% so that the AEG% p.a. line has moved to co-inside with the Y-Axis.

Later, readers will find that the reason is that this figure provides a 4% p.a. distance between AEG% p.a. and a repayment period of 25 years at outset, regardless of what the nominal rate of interest is and assuming that the true interest rate will average out at what was found to be the usual rate of around 3% p.a. for prime loans in a well managed economy. That is before central banks lowered interest rates too far at the start of this century. They are trying to find a way to get interest rates 'back to normal' without causing problems with home buyers and businesses. They have started to think that curbing the amount lent at outset is a good idea.

If central banks had not reduced interest rates the way they did, and if the entry cost remained fairly stable as nominal interest rates vary, the size of new loans would be correspondingly steady, not rising much as interest rates fall with falling inflation.

But what lenders did and maybe still do, is to reduce the entry cost when nominal interest rates r% fall. That is high risk but that is what lenders often do right now. As interest rates fall they drop the entry cost, (risky), push up the size of new loans, (risky), and inflate property values making them likely to fall later - also risky. This is a high risk way to calculate the entry cost.

As already explained, for a standing loan to exist, P / L = Constant. That is saying that the payments 'P p.a.' must rise or fall at the same pace as L.

From Equation (i) which was:

To create a standing loan P% has to be a constant.

P% = K

where K has some constant value.

The 'X' is then on the Y-axis at P% = r%. See FIG 0

In the next table the interest r% = 7% as before but P% starts at 6% which in this example is 6,000 p.a. In a year, the loan ‘L’ rises by 1% p.a.

For there to be a standing loan the payments 'P p.a.' must catch up at the end of the year. In order to do that, 'P p.a.' must rise by 1% .

FIG 1 - Standing Loan when e% = 0% and e% = 1%

We can move the 'X' another 1% below r% making P% = 5% p.a. or 5,000 in this example, as in Table 2 below. This gives a third ‘X’ on the chart in which the loan rises by 2% and so the payments 'P' must rise by 2% at year's end meaning that e% has to go to 2% p.a. to catch up. See Table 2 and FIG 2 below.

This can be repeated for as many values of the entry cost as we wish.

This also works. The loan is rising as fast as the payments. This time the 'X' is higher at 8% because it is to the left of the Y-Axis. See FIG 3

If the loan is being repaid the loan gets smaller compared to the payments. This means that P% rises every year. In the final year P% is more than100% of L because if the final payment was equal to L (P% = 100%) that would pay all of the capital but none of the interest added in that year. In the case of a 5-year loan the repayments table might look like this:

This way it gets easier for most people to repay every year and so the arrears rate is low. This is a key feature of a safe repayments schedule.

The gap between the rate of increase in the payments, e% p.a. and the rate of increase of NAE, AEG% p.a. may narrow but the payments will not leap upwards and could if necessary be increased a little - but tests on past data using spreadsheets show that this is not likely to be necessary.

IMPLEMENTATION

This is a good way to start making the transition from the LP Model to the ILS Model. Lenders and borrowers keep on doing what they always do, but when there is a serious problem with a rise in interest rates, there is an escape hatch - move the 'X' to the right. Payments will not rise till the end of the year and then the increase will be small.

SUMMARY SO FAR

This means that the standing loan line forms an equal sided triangle (same length on both major axes) and it means that it crosses the vertical and horizontal axes at the same figure of r%.

We have also placed an AEG% (Average Earnings / Incomes Growth) line on the chart. We know that this line moves to the left and to the right as the value of AEG% p.a. changes.

We know that we do not want the AEG% p.a. line to get too close to the 'X', especially in the early years. And we want the 'X' to be far enough to the left of the AEG% p.a. line to protect any borrowers whose incomes are not rising as fast as average and to remove as much as possible of the threat of Payments Fatigue. 4% p.a. separation seems to be about right based on past data for arrears using the LP Model in the UK where the author lived until the 1990s.

PART 2

Here the letters, C%, D%, and I%, have been added to the chart.

The objective now is to find an equation that gives us the value of P% for position 'X' on the chart.

So we have three variables to consider: 'C%', 'D%', and 'I%', as seen in FIG 5 above, and again, in FIG 6 below.

In FIG 6 we can link all three variables together with equilateral triangles, like this:

Hence by adding up the vertical distances we can see that:

P% = C% + D% + I% - The Safe Entry Cost and Management Equation

It can be used as a management tool for managing the level of repayments, keeping them in a safe and low risk area of the chart.

WHAT WE HAVE FOUND

There are no debt repayment schedules on earth which have no value of

'e%' or no value of 'P%'. Since all debt repayment schedules have a value 'P%' and

a value of e%, they also have a value for 'C%', 'D%', and 'I%'.

If 'D% p.a.' is allowed to go negative and stay negative for very long in the early years, before the cost to earnings has reduced significantly, then there will be a lot of arrears.

In short I calculate the following year's payments by adjusting D% first based on the latest known value of I%. For every 1% change in I% the spreadsheet adjusts D% by 1% in the opposite direction.

For a fairly stable entry cost of 8.5% consuming, say 30% of the earnings of a single borrower, we get a loan of 3.5 times annual earnings. It is assumed that lenders will select net earnings after deducting commitments like credit card payments and other loans...

Exactly how they apply this equation is up for discussion.

But clearly it is risky to lend a lot more and it is not necessary to lend a lot less.

Property loans will have a value which rises with NAE. This meets the requirements given for a financially stable property sector which is also low in arrears.

The payments 'P' rise annually as fast as NAE rises less the scheduled reductions of D% p.a. But macro-economically the lending sector as a whole comprises new and old borrowers so the amount of aggregate earnings devoted to mortgage repayments will tend to rise alongside NAE. Spending patterns will not be altered much by rising or falling AEG% p.a. The cost of loan repayments will not leap up when interest rates rise by a percentage point or more.

The entire property sector will be financially stable and will not divert aggregate spending as the rate of AEG% p.a. and the level of prices inflation varies nominal rates of interest.

Having all costs, payments, earnings, and values able to rise at a similar percentage rate compared to what they would otherwise be, is a condition to be met for creating a financially stable economy.

So ILS Mortgages can help to create financial stability / remove a significant amount of financial instability.

To find the entry value of 'C%' for a given total repayment period please visit Waghorn's Equations

OTHER LINKS

-----------------------------------

The basic economics and my group's theory of the origins of financial instability, is given on the Home Page of the Main Blog, and is being written more fully as a NUMBER OF BOOK VOLUMES of which this mathematics will be a key part of the overall book.

Currently the title will be 'A tract on Financial Stability' or the short version will omit this and will be called 'A Short Tract on Financial Stability'.

There is this page on NEW FINANCIAL PRODUCTS RESULTING which is based upon this maths.

Some of the research done on past true rates of interest can be found on the three pages starting with this one. The third page explains why interest rates are distorted and currently low.

Section #1 of these volumes will be about financial stability in the savings and loans sector.

Sections #2 and #3 of the book are covered quite well in outline on www.fin24.com in the later essays. There is a guide to those essays here.

Section #2 deals with problems of money creation, including the cause of unstable interest rates, booms and busts resulting, and a suggested remedy. A lot of research is currently under way on this topic and is outlined, but this book probably leads the way.

Section #3 deals with currency price instability, and a suggested remedy.

This maths page is a part of Section #1 or it may be an Appendix to Section #1.

Various attempts have been made to write the opening pages of the book on this website - but they are all now out of date.

Ongoing re-writes, updates and additional material are noted on the LATEST UPDATES page.

GENERAL EQUATIONS

FOR THE REPAYMENT OF DEBT

DEFINITIONS - for later reference only

ILS Models - The Ingram Lending and Savings Models for safe lending and savings.

r%, the nominal rate of interest, is split into two parts:

ILS Models - The Ingram Lending and Savings Models for safe lending and savings.

· NAE - National Average Earnings / Incomes

· AEG% p.a. - The rate of Growth of NAE.

· AEG% p.a. stands for the Average Earnings Growth % p.a.

· r% - the rate of interest also known as the nominal rate of interest.

CONVENTION

Sometimes it simplifies equation reading and writing if the suffix ‘p.a.’ is dropped.

r%, the nominal rate of interest, is split into two parts:

- r% = AEG% + I% ---(a)

- I% is called the TRUE rate of interest, or the marginal rate above AEG%

- r% = AEG% +I% ....(b)

- e% = the annual rate of increase in the debt servicing payments, P p.a.

There is no rule which says that the repayments P p.a. have to be fixed.

- D% = AEG% - e% ...........(c)

Where ‘D%’ is the rate of Payments Depreciation. D% p.a. is how much less quickly the payments rise than AEG%.

NOTE: There is no rule that says AEG% p.a. should be the index of choice. A wages index has often been used in its place in back-tests done with a spreadsheet. Some may prefer to use the median rate of increase. Every lender should do tests on past data to see which index works best for them. In some places, India for example, there are many provinces with differing real rates of interest or true rates of interest. In some provinces and in some nations true rates of interest can be much higher than in others. This affects the amount that can be lent safely.

Recently, in 2020, it has come to the attention of the writer that highly negative rates of interest have been suggested as a way forward to come out of the Covid-19 crisis. This idea has not yet been tested on the spreadsheets or the mathematical theory. A study will be made shortly. There may be options to consider when for example the negative rate of interest is reducing the true principle or the nominal principle sum owed. Would the lender make payments on behalf of the borrower at such times? How would that affect cash flows? What is proposed for the usual annuity / LP model?

Recently, in 2020, it has come to the attention of the writer that highly negative rates of interest have been suggested as a way forward to come out of the Covid-19 crisis. This idea has not yet been tested on the spreadsheets or the mathematical theory. A study will be made shortly. There may be options to consider when for example the negative rate of interest is reducing the true principle or the nominal principle sum owed. Would the lender make payments on behalf of the borrower at such times? How would that affect cash flows? What is proposed for the usual annuity / LP model?

- P% = P/L x 100% so it is the payment P expressed as a percentage of the loan L

- C% = the capital element - the rate of repayment of NAE - something not to be understood yet.

MAIN MATHS

PART 1

Creating a Risk Management Chart

DEFINITIONS FOR IMMEDIATE USE

P = the current level of annual payments p.a.

Note: The definition of payments is the sum paid to service the loan. P may or may not be enough to reduce the loan or its value. It is just a symbol representing the payments.

Note: The definition of payments is the sum paid to service the loan. P may or may not be enough to reduce the loan or its value. It is just a symbol representing the payments.

L = the debt / loan / mortgage value

P% p.a. is the annual percentage of the debt 'L' that is being paid by money payments 'P' p.a.

I often drop the 'p.a.' part as this is understood. This is easier to read that way:

I often drop the 'p.a.' part as this is understood. This is easier to read that way:

P

P% = ---- x 100% --------------- (i)

L

I could have written:

P p.a.

P% p.a. = --------- x 100%

L

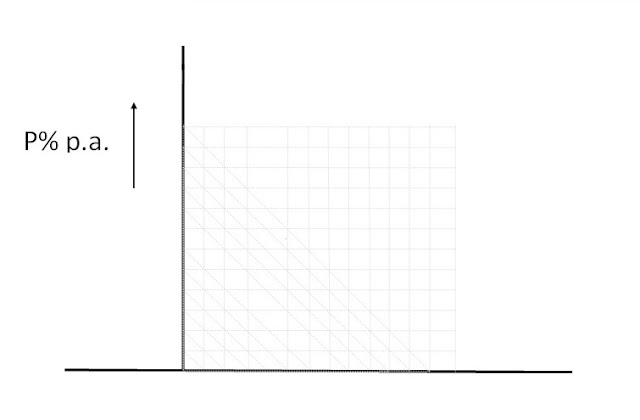

Let's place P% p.a. on the Y-Axis (Vertical Axis) of a chart.

CONVENTION:

$, €, £, ¥ symbols are not necessary. The numbers work in any currency.

EXAMPLE FOR USING P%

If P = 7 p.a. and L = 100, then:

P% p.a. = 7% p.a.

The lending industry usually refers to the traditional repayments (annuity) model as a Level Payments (LP) model even though an interest rate change creates a new level of payments.

For the annual payment 'P p.a.' needed to service the loan to be fixed and level, the nominal interest rate r% has to be fixed.

STANDING LOANS WITH LEVEL PAYMENTS

Let r% = Nominal Interest (the rate of interest).

If interest r% = 7% then the interest added to a loan of 100 is 7 in any currency, making a loan of 107 at year's end.

If P% = 7% then every year the payment P = 7. This removes the interest added reducing the year's end balance from 107 to 100, leaving the balance unchanged at 100 as before. This is called a standing loan. It never gets repaid. It never rises either.

In general, there is a standing loan if P% = r%.

Now for something a little different.

We are deriving the General Equation for repayments of any kind of regular payments loan. For this there is a different definition of a standing loan. We will come to that shortly.

We do not have to specify that the repayments will be level. We can say that they may rise every year at, say e% p.a.

e% p.a. = the percentage rate at which debt servicing payments 'P' p.a. will increase every year.

If ‘e’ is negative the payments are falling.

Example: if P = 100 and e% = 3% p.a. in the following year the new value of P = 103, in any currency.

We can add e% as the X-Axis.

Now we can place an 'X' on the chart such that 'X' has a value on the 'P% p.a.' axis and another vale on the 'e% p.a.' axis.

The position of the 'X' describes the current value of 'P% and 'e%'

The initial place of the 'X' on the chart can be selected by the lender. The 'X' does not have to be on the vertical Y-axis. The 'X' can be placed anywhere. But where is it safe to put it?

When we place the ‘X’ we must know that the payments should not increase as fast as the rate at which the borrowers’ incomes are rising:

e% p.a., the rate of increase of 'P p.a.' should be less than the rate of increase of a typical borrower's earnings, Average Earnings Growth, AEG% p.a..

e% < AEG% p.a.

So we draw a line on the chart to represent AEG% p.a.

Here, the 'X' is shown to the left of the AEG% p.a. line.

As just mentioned, the exact definition of AEG% p.a. is something that needs careful thought. But as long as the 'X' is far enough to the left of the AEG% line, as long as the difference between e% and AEG% p.a. is large enough the great majority of borrowers will have earnings which are rising faster than the payments 'P p.a.' are rising. AEG% p.a. is the rate at which National Average Earnings, NAE, are rising.

FIRSTLY - RISK MANAGEMENT

The further to the left of the AEG% line that the 'X' is placed, the fewer borrowers will get into arrears.

If NAE was rising at 4% p.a. and interest rates were fixed, which is about how things may have worked out in the 1900's when economies were not in crisis, this 4% difference between AEG% p.a. (4%) and e% (0%) would put e% p.a. at 4% p.a. to the left of the AEG% p.a. line no matter where that AEG% line was at the time. In the past this was enough to keep arrears rates under good control. We call this figure the rate of Payments Depreciation because it makes the payments cost less every year.

Of course, most payments are made monthly. Readers should divide the annual figure by twelve to get the monthly payment.

At 4% p.a. payments depreciation, at the end of the first 3 three years the monthly cost would be almost 12% less than NAE.

If NAE was rising by less than 4% p.a. then payments 'P' per annum, or the new monthly payments asked for, would fall every year.

With the LP model and a fixed interest rate, NAE% p.a. MUST be rising by 4% p.a. to get this outcome. But no one controls the rate of growth of NAE, the rate of Average Earnings Growth.

With the LP model and a fixed interest rate, NAE% p.a. MUST be rising by 4% p.a. to get this outcome. But no one controls the rate of growth of NAE, the rate of Average Earnings Growth.

If we can create a rule that payments depreciation must always be a positive figure then we do not need to worry about the rate at which average earnings are rising. Read on, maybe that can be done.

SECONDLY

We need to know that the 'X' is high enough to repay the loan. If the 'X' lies on the Y-Axis, meaning that the payments are scheduled to be level and not rising or falling, it needs to be above the rate of interest 'r%'. This means that some of the capital is being repaid.

If we move the 'X' off the Y-Axis, how will we know if it is high enough to repay the loan?

We need to find a standing loan line at which level the loan will never be repaid. The 'X' needs to be high enough above this line to repay the loan in the time available, say 25 years.

FIG 1 Ingram's Risk Management Chart

This is what the standing loan line looks like. Why it looks like that is the next thing to find out. See FIG 1

THE FULL CHART

This chart has two Axes, two straight dashed lines, one at 45 degrees slope representing a standing loan line and one dashed vertical line representing the current rate of AEG% p.a., and an 'X' whose position on the chart describes the current state of a specific regular payments loan.

THE FULL CHART

This chart has two Axes, two straight dashed lines, one at 45 degrees slope representing a standing loan line and one dashed vertical line representing the current rate of AEG% p.a., and an 'X' whose position on the chart describes the current state of a specific regular payments loan.

The position of the 'X' describes the current value of P% and of e%. And the position of the 'X' has a visible horizontal distance from the AEG% p.a. line and a visible vertical distance from the standing loan line - two safety margins to be aware of. Later, these distances will be given names and included in the risk management equation.

USING THE CHART

'X' has a value of e% and a value of P% - as any debt repayments schedule has.

So there is always a position of the 'X' which can represent ANY regular repayments schedule for any kind of loan. Any place on the chart has a value for P% and a value for e%, both being p.a.

Any position on the chart has two safety margins.

The vertical and horizontal safety margins for any repayments schedule at any point in time can be read off the chart. Just find the e% and the P% values and place the 'X' where it belongs.

In the above FIG 1 example the 'X' lies to the left of the AEG% p.a. line and above the standing loan line, so that the debt is being repaid safely. The area to the left of the AEG% p.a. line and above the standing loan line is the safe area for placing the 'X'. The further the 'X' is placed from these two lines the safer the repayments schedule will be.

These two distances are margins of safety because if the interest rate changes or the value of AEG% p.a. changes either or both of those two distances may be reduced unless the position of the 'X' is actively managed in some way. We will come to that later. As long as the 'X' remains in the safe area and it does not jump upwards suddenly the loan repayments will be comfortable for borrowers.

As long as 'e%' remains to the left of the AEG% line and above the standing loan line the debt will eventually be repaid.

This raises a number of 'How to' questions including how the lender will manage its cash flows. Those are questions to be addressed later.

As long as 'e%' remains to the left of the AEG% line and above the standing loan line the debt will eventually be repaid.

This raises a number of 'How to' questions including how the lender will manage its cash flows. Those are questions to be addressed later.

FINDING THE STANDING LOAN LINE

In the next chart, an 'X' is placed at r% and represents a standing loan. The 7% interest is being repaid using e% = 0% (Level Payments). To repay the loan the 'X' has to be higher than the standing loan line - in this case it must be above r%, for example the position 'X1' would repay the loan as long as r% did not rise too much.

{kind=link}

To repay in 25 years 'X1' would have a value of around 8.5% p.a. Those used to be typical figures before central banks in the developed economies reduced interest rates to below normal levels from around the year 2000 onward.

When the interest rate rises then the standing loan line also rises. With the LP model where the 'X' must stay on the vertical axis, then to repay the debt on schedule the ‘X’ jumps up to a new level. I.e. the annual and monthly cost of the loan servicing payments jumps up. The change is not scheduled and it may create arrears problems.

When the interest rate rises then the standing loan line also rises. With the LP model where the 'X' must stay on the vertical axis, then to repay the debt on schedule the ‘X’ jumps up to a new level. I.e. the annual and monthly cost of the loan servicing payments jumps up. The change is not scheduled and it may create arrears problems.

A possible alternative would have been for the ‘X’ to move to the right and stay above the new standing loan line. Maybe the AEG% p.a. line has also moved to the right because higher interest rates are often linked to higher levels of AEG% p.a. In any case, there is likely to be room to move the 'X' to the right. Doing that would reduce the level of arrears which normally rises sharply when interest rates increase. We will look at how that appears on the chart later.

DEFINING THE STANDING LOAN LINE

The standing loan line is a line which, if the 'X' is placed anywhere on it, the loan will never be repaid. If the 'X' happens to be on the standing loan line then the value of the debt 'L' will be rising at the exact same pace as the payments 'P' are rising.

This means that the ratio P/L never changes and so the value of P% p.a. never changes. It stands still. Normally P% p.a. rises every year as the loan gets repaid. This is because as 'L' reduces as the result of the payments 'P', the ratio P/L rises.

Remember, P% = P/L x 100% so if P/L rises so does P%. But if the loan and the payments are both rising at the exact same pace, then the ration P/L never changes and the loan will never get repaid. There will always be a new 'P' and a new 'L' remaining.

It is like a race in which the payments increases are chasing the loan size 'L' increases. If both are rising at the same rate neither side wins. It is a dead heat.

THE CASE WHEN e% IS NEGATIVE

In maths there is usually a case when variables go negative. It is the same on the charts. What happens to the standing loan line and to the 'X' if the loan is still to be repaid?

Let us place AEG% p.a. on the Y-Axis. AEG% p.a. is not rising. If trouble is to be avoided, both the Loan Size 'L' and the Payments 'P' must be falling. If payments depreciation is say, 4% p.a. and AEG% p.a. = 0%, this means that e% p.a. = -4% p.a.

In this case we have to extend the standing loan line to the left of the Y-Axis:

The 'X' is above the standing loan line but to the left of the Y-Axis. The mortgage is being repaid even though the payments are falling every year. In this particular illustration, the level of payments 'P' is not very high because of the very low nominal rate of interest of 3%. That is what happens when inflation and AEG% p.a. are very low. A low interest rate moves the standing loan line down.

Here is a spreadsheet illustrating how that might work. In the table and on the chart above, AEG% = 0% so that the AEG% p.a. line has moved to co-inside with the Y-Axis.

This is how that position of the ‘X’ on the above chart looks in tabulation form.

As shown in this table, (with AEG% = 0% and e% = - 4% p.a. in this example), the payments are falling every year and the debt is falling even faster because the 'X' is above the standing loan line.

As shown in this table, (with AEG% = 0% and e% = - 4% p.a. in this example), the payments are falling every year and the debt is falling even faster because the 'X' is above the standing loan line.

In order to simplify this repayments table, all transactions occur at year's end.

The balance at the end of each year is carried forward to the start of the next year.

On this schedule the debt is paid off in the 25th year.

Without wishing to explain this right now, please note that the repayments start at 8,455 p.a.

Given this initial loan of 100,000, this means that P% starts at 8.455% p.a.

This starting cost is called the Entry Cost.

This entry cost is not far from P% = 8.5%.

P% = 8.5% would be about the right entry cost figure to repay the same loan in the same 25 years, if the nominal rate of interest r% was fixed at 7% p.a. and the repayments were level.

For some reason which the reader does not yet know, P% = 8.5% p.a. is a kind of 'sweet entry cost' for the repayment of a home loan over 25 years. Whatever the nominal rate of interest r% may be, this is normally a good (fairly safe) level at which to start the repayments.

I am removing this because it is more economics theory than what readers need to know and it may reduce trust in the mathematics which is just maths and not assumptions.

If central banks had not reduced interest rates the way they did, and if the entry cost remained fairly stable as nominal interest rates vary, the size of new loans would be correspondingly steady, not rising much as interest rates fall with falling inflation.

NOW GOING BACK TO

FINDING THE STANDING LOAN LINE

To find out where that standing loan line may be we have to do some thinking.

As already explained, for a standing loan to exist, P / L = Constant. That is saying that the payments 'P p.a.' must rise or fall at the same pace as L.

From Equation (i) which was:

P

P% = ---- x 100% --------------- (i)

L

To create a standing loan P% has to be a constant.

P% = K

where K has some constant value.

The usual Level Payments system is special case. It is when e% = 0%. Neither P nor L changes from year to year. The rate of increase of both P and L is zero. The ratio P/L = is a constant. It is when P% = r% = K, a constant. See Table 0 below.

Table 0: The Standing loan where r% = 7% and e% = 0% p.a.

ADD

|

SUBTRACT

| ||||

Yr

|

LOAN

|

INTEREST

|

PAYMENT

|

BALANCE

|

P%

|

1

|

100 000

|

7 000

|

7000

|

100 000

|

7,00%

|

2

|

100 000

|

7 000

|

7000

|

100 000

|

7,00%

|

3

|

100 000

|

7 000

|

7000

|

100 000

|

7,00%

|

The 'X' is then on the Y-axis at P% = r%. See FIG 0

FIG 0

In the next table the interest r% = 7% as before but P% starts at 6% which in this example is 6,000 p.a. In a year, the loan ‘L’ rises by 1% p.a.

For there to be a standing loan the payments 'P p.a.' must catch up at the end of the year. In order to do that, 'P p.a.' must rise by 1% .

Now we see, in Table 1, as expected, that P% = a constant 6%. Every year. P% = 6% See Table 1 below.

Table 1: e% = 1% p.a. Payments rise 1% every year.

ADD

|

SUBTRACT

| ||||

Yr

|

LOAN

|

INTEREST

|

PAYMENT

|

BALANCE

|

P%

|

1

|

100 000

|

7 000

|

6 000

|

101 000

|

6,00%

|

2

|

101 000

|

7 070

|

6 060

|

102 010

|

6,00%

|

3

|

102 010

|

7 141

|

6 121

|

103 030

|

6,00%

|

Fig 1 shows this on the Chart at position ‘X1’. Now we have two points on the graph, both representing a standing loan.

FIG 1 - Standing Loan when e% = 0% and e% = 1%

We can move the 'X' another 1% below r% making P% = 5% p.a. or 5,000 in this example, as in Table 2 below. This gives a third ‘X’ on the chart in which the loan rises by 2% and so the payments 'P' must rise by 2% at year's end meaning that e% has to go to 2% p.a. to catch up. See Table 2 and FIG 2 below.

Table 2: e% = 2% p.a. P% = a constant 5%

ADD

|

SUBTRACT

| ||||

Yr

|

LOAN

|

INTEREST

|

PAYMENT

|

BALANCE

|

P%

|

1

|

100 000

|

7 000

|

5 000

|

102 000

|

5,00%

|

2

|

102 000

|

7 140

|

5 100

|

104 040

|

5,00%

|

3

|

104 040

|

7 283

|

5 202

|

106 121

|

5,00%

|

On the Risk Management Chart this is how that looks - see X2

FIG 2 Standing Loan at e% = 0%, 1%, and 2% p.a.

This can be repeated for as many values of the entry cost as we wish.

Every time the ‘X’ drops by 1%, it has to move 1% to the right to create a standing loan.

What if e% is negative?

In the next table e% = -1% p.a.

P% = constant at 8%.

Table 3: e% = -1% p.a.

ADD

|

SUBTRACT

| ||||

Yr

|

LOAN

|

INTEREST

|

PAYMENT

|

BALANCE

|

P%

|

1

|

100 000

|

7 000

|

8 000

|

99 000

|

8,00%

|

2

|

99 000

|

6 930

|

7920

|

98 010

|

8,00%

|

3

|

98 010

|

6 861

|

7 841

|

97 030

|

8,00%

|

This also works. The loan is rising as fast as the payments. This time the 'X' is higher at 8% because it is to the left of the Y-Axis. See FIG 3

FIG 3

EQUILATERAL TRIANGLE

Hence the Standing Loan Line forms an equal sided (equilateral) right angled triangle. The two equal sides of the triangle are the two major axes, and the standing loan line is the hypotenuse.

Because the two sides are of equal length, the standing loan line crosses both the Y-axis and the X-axis at the same value, r% as shown.

NORMALLY P% RISES

If the loan is being repaid the loan gets smaller compared to the payments. This means that P% rises every year. In the final year P% is more than100% of L because if the final payment was equal to L (P% = 100%) that would pay all of the capital but none of the interest added in that year. In the case of a 5-year loan the repayments table might look like this:

Table 4 - A 5 year loan see P% rising every year and ending at over 100%

ADD

|

SUBTRACT

| ||||

Yr

|

LOAN

|

INTEREST

|

PAYMENT

|

BALANCE

|

P%

|

1

|

100 000

|

7 000

|

24 389

|

82 611

|

24,39%

|

2

|

82 611

|

5 783

|

24 389

|

64 005

|

29,52%

|

3

|

64 005

|

4 480

|

24 389

|

44 096

|

38,11%

|

4

|

44 096

|

3 087

|

24 389

|

22 794

|

55,31%

|

5

|

22 794

|

1 596

|

24 389

|

0

|

107,00%

|

In the final year the loan outstanding is 22,794 but interest of 1,596 also has to be repaid. So P% is more than 100% in this last year.

A SAFE PLACE FOR THE 'X'

To make a loan affordable and safe the 'X' has to be sufficiently above the standing loan line so that it gets repaid and it has to be sufficiently to the left of the AEG% p.a. line so that the payments increase more slowly than incomes do.

This way it gets easier for most people to repay every year and so the arrears rate is low. This is a key feature of a safe repayments schedule.

Since no individual's income rises at the exact AEG% p.a. rate, and since there could be some discussion about how the AEG% figure is calculated, the 'X' must be placed some distance to the left of the AEG% p.a. line.

SETTING THE MARGINS

The objective of reducing the rate of increase in the payments below AEG% p.a. is to prevent what lenders call Payments Fatigue, for the majority, (say 95% or more), of borrowers and to ensure that the payments are affordable.

With the traditional LP model when interest rates rise by 1% the cost of the repayments may jump up by 10% or more. See Table 5.

Table 5 - The interest rate sensitivity of Repayments and Loan Sizes offered by LP over 25 years.

This also causes LP Lenders to lend more, inflating property prices and making them vulnerable when interest rates rise and the repayments jump up and become unaffordable. Mass repossessions can crash property values further and ruin the lenders that cannot recover their capital by selling the properties. The borrowers may all have been credit-worthy, but now, in these conditions, unemployment threatens and families are being destroyed.

This also causes LP Lenders to lend more, inflating property prices and making them vulnerable when interest rates rise and the repayments jump up and become unaffordable. Mass repossessions can crash property values further and ruin the lenders that cannot recover their capital by selling the properties. The borrowers may all have been credit-worthy, but now, in these conditions, unemployment threatens and families are being destroyed.

Source of the table - Ingram Spreadsheet for 25 years LP Model.

With the new Ingram Lending and Savings (ILS) repayments model, even if interest rates had risen by 1% and the ‘X’ were to be moved 1% to the right of the Y-Axis, at e% = 1% p.a. it would be a decade before the payments reached that same level as those demanded by the LP model after a 1% rise in r%. By that time borrowers would have had plenty of increases in their earnings and would be easily able to afford that 10% higher repayment cost.

Because the 'X' would still be the same distance above the new, higher, standing loan line, calculations show that the loan will still be repaid almost on schedule.

Figure 4 - IMPLEMENTATION

Table 5 - The interest rate sensitivity of Repayments and Loan Sizes offered by LP over 25 years.

Source of the table - Ingram Spreadsheet for 25 years LP Model.

With the new Ingram Lending and Savings (ILS) repayments model, even if interest rates had risen by 1% and the ‘X’ were to be moved 1% to the right of the Y-Axis, at e% = 1% p.a. it would be a decade before the payments reached that same level as those demanded by the LP model after a 1% rise in r%. By that time borrowers would have had plenty of increases in their earnings and would be easily able to afford that 10% higher repayment cost.

Because the 'X' would still be the same distance above the new, higher, standing loan line, calculations show that the loan will still be repaid almost on schedule.

Figure 4 - IMPLEMENTATION

The gap between the rate of increase in the payments, e% p.a. and the rate of increase of NAE, AEG% p.a. may narrow but the payments will not leap upwards and could if necessary be increased a little - but tests on past data using spreadsheets show that this is not likely to be necessary.

IMPLEMENTATION

This is a good way to start making the transition from the LP Model to the ILS Model. Lenders and borrowers keep on doing what they always do, but when there is a serious problem with a rise in interest rates, there is an escape hatch - move the 'X' to the right. Payments will not rise till the end of the year and then the increase will be small.

SUMMARY SO FAR

So far we have established the framework

of the Risk Management Chart, the fact that we can draw a standing loan line

which slopes downwards at 45 degrees.

This means that the standing loan line forms an equal sided triangle (same length on both major axes) and it means that it crosses the vertical and horizontal axes at the same figure of r%.

We have also placed an AEG% (Average Earnings / Incomes Growth) line on the chart. We know that this line moves to the left and to the right as the value of AEG% p.a. changes.

We know that we do not want the AEG% p.a. line to get too close to the 'X', especially in the early years. And we want the 'X' to be far enough to the left of the AEG% p.a. line to protect any borrowers whose incomes are not rising as fast as average and to remove as much as possible of the threat of Payments Fatigue. 4% p.a. separation seems to be about right based on past data for arrears using the LP Model in the UK where the author lived until the 1990s.

PART 2

Derivation of the Main Equation

P% = C% + D% +

I%

All variables in the equation are p.a.

Both 'P%' and 'C%' are a percentage of the loan

balance 'L'.

In FIG 5, below, all four variables are displayed on one chart.

FIG 5 - All Variables

Displayed

Here the letters, C%, D%, and I%, have been added to the chart.

The objective now is to find an equation that gives us the value of P% for position 'X' on the chart.

NOTE the precise definition of D%:

D% = AEG% - e% - (ii) - all are p.a.

Or if you prefer, this can be re-arranged:

e% = AEG% - D% - (iii)

This is the mathematical way to say that the rate of increase in the annual payments P p.a. is D%

p.a. less than AEG% p.a. It is shown on the chart above as D%.

TRUE INTEREST 'I%' - THE DEFINITION

The nominal rate of interest has two components:

REMINDER

The true interest rate ‘I%’ is the marginal rate above

AEG% p.a.

By this definition:

r% = AEG% + I%

We can re-write this equation as:

I% = r% - AEG% ............(iv)

I% is also shown on the above chart. See the double headed arrow just above the X-axis. That distance is r% - AEG%. And that is I% the definition of I%.

So we have three variables to consider: 'C%', 'D%', and 'I%', as seen in FIG 5 above, and again, in FIG 6 below.

In FIG 6 we can link all three variables together with equilateral triangles, like this:

FIG 6 - Derivation of the General Equation for P%

Two small equal-sided

right angle triangles have been added.

One triangle has two equal sides of length I%, and above that,

One triangle has two equal sides of length D%.

In each case there is a horizontal line and an equal length vertical line.

Hence by adding up the vertical distances we can see that:

P% = C% + D% + I% - The Safe Entry Cost and Management Equation

IMPORTANT NOTE:

This equation can be used to estimate a safe entry cost by

ensuring that the variables 'C%' and 'D%' are large enough at outset to cope with any expected variations in AEG and r%.

It can be used as a management tool for managing the level of repayments, keeping them in a safe and low risk area of the chart.

WHAT WE HAVE FOUND

All debt repayment schedules have these three elemental parts. At any point in time they all have a value of 'I%' and 'D%' and 'C%'.

The Safe Entry Cost Equation is a general equation for lending and risk management. Arrears risk is managed by managing the position of the 'X' on these charts and hence the changing values of 'C%' and 'D%'.

We can take over any kind of loan and start to manage the 'D%' and 'C%' variables to bring it to a safe conclusion - provided that the D% and the C% are big enough to cope at the time that we intervene.

The Safe Entry Cost Equation is a general equation for lending and risk management. Arrears risk is managed by managing the position of the 'X' on these charts and hence the changing values of 'C%' and 'D%'.

We can take over any kind of loan and start to manage the 'D%' and 'C%' variables to bring it to a safe conclusion - provided that the D% and the C% are big enough to cope at the time that we intervene.

In my spreadsheet tests on historic data and on experimental data I have automated the chaning value of D% so that for every 1% change in the value of I% D% is changed by 1% in the opposite direction.

This means that P% is not disturbed by changes in the value of I% and neither is C% altered.

Remember,

P% = C% + D% + I% defines where the 'X' is on the chart. P% is the height and the cost and if D% varies when I% varies so be it.

What we know is that I% varies less than r% because a lot of r% is compensation for inflation of prices and wages. r% = AEG% + I% so a jump in AEG% that leads to a similar rise in r% will have relatively little effect on I%.

If 'D% p.a.' is allowed to go negative and stay negative for very long in the early years, before the cost to earnings has reduced significantly, then there will be a lot of arrears.

MANAGING THE REPAYMENTS

It is time to look at how to manage these variables safely and to find the safe minimum values for C% and D% and the envelope within which it can work.

That will be done on other pages of this website - as yet not written. But it has all been worked out and is waiting to be published. There are examples of what can be achieved on some linked pages. For example:

NEW FINANCIAL PRODUCTS RESULTING - TO BE EDITED BEFORE BEING MADE AVAILABLE AGAIN

and

There is a way to estimate the upper and lower limits of I% which concludes that I% always averages somewhere between 1% and 4% over the long term in order to create a limited and manageable rate of inflation.

By starting with an entry price P% that assumes that I% will average out at 3%, this means that D% = 4% should be enough in most cases to prevent P% from having to leap upwards which is what happens with LP mortgages using variable rates of interest.

Here is why:

P% = C% + D% + I%

Let I% rise by a maximum of 4% (that would take it to 7%) and let it remain at that high level. The only reason why that can happen is because the risks of lending, the level of non-performing loans and write-offs would cost lenders around 4% p.a. Or because of a monopoly lender able to charge whatever it likes. However, if this were to happen:

For P% and for C% to be unaffected so that the loan is repaid on schedule, D% must fall by 4% to zero. This would be stressful for many borrowers.

So a typical safe loan might be given by:

P% = C% of 1.5% (repays in around 25 years) + D% of 4% + I% expected average 3% as opposed to the current rate.

So P% Safe Entry Cost is given by:

P% = 1.5% + 4% + 3% = 8.5%

This is the entry cost used in almost all of my spreadsheet tests of this new ILS Model for Housing Finance, using historic data and various inputted extreme data to see what happens.

It is time to look at how to manage these variables safely and to find the safe minimum values for C% and D% and the envelope within which it can work.

NEW FINANCIAL PRODUCTS RESULTING - TO BE EDITED BEFORE BEING MADE AVAILABLE AGAIN

and

There is a way to estimate the upper and lower limits of I% which concludes that I% always averages somewhere between 1% and 4% over the long term in order to create a limited and manageable rate of inflation.

By starting with an entry price P% that assumes that I% will average out at 3%, this means that D% = 4% should be enough in most cases to prevent P% from having to leap upwards which is what happens with LP mortgages using variable rates of interest.

Here is why:

P% = C% + D% + I%

Let I% rise by a maximum of 4% (that would take it to 7%) and let it remain at that high level. The only reason why that can happen is because the risks of lending, the level of non-performing loans and write-offs would cost lenders around 4% p.a. Or because of a monopoly lender able to charge whatever it likes. However, if this were to happen:

For P% and for C% to be unaffected so that the loan is repaid on schedule, D% must fall by 4% to zero. This would be stressful for many borrowers.

So a typical safe loan might be given by:

P% = C% of 1.5% (repays in around 25 years) + D% of 4% + I% expected average 3% as opposed to the current rate.

So P% Safe Entry Cost is given by:

P% = 1.5% + 4% + 3% = 8.5%

This is the entry cost used in almost all of my spreadsheet tests of this new ILS Model for Housing Finance, using historic data and various inputted extreme data to see what happens.

For a fairly stable entry cost of 8.5% consuming, say 30% of the earnings of a single borrower, we get a loan of 3.5 times annual earnings. It is assumed that lenders will select net earnings after deducting commitments like credit card payments and other loans...

Exactly how they apply this equation is up for discussion.

But clearly it is risky to lend a lot more and it is not necessary to lend a lot less.

Property loans will have a value which rises with NAE. This meets the requirements given for a financially stable property sector which is also low in arrears.

The payments 'P' rise annually as fast as NAE rises less the scheduled reductions of D% p.a. But macro-economically the lending sector as a whole comprises new and old borrowers so the amount of aggregate earnings devoted to mortgage repayments will tend to rise alongside NAE. Spending patterns will not be altered much by rising or falling AEG% p.a. The cost of loan repayments will not leap up when interest rates rise by a percentage point or more.

The entire property sector will be financially stable and will not divert aggregate spending as the rate of AEG% p.a. and the level of prices inflation varies nominal rates of interest.

Having all costs, payments, earnings, and values able to rise at a similar percentage rate compared to what they would otherwise be, is a condition to be met for creating a financially stable economy.

So ILS Mortgages can help to create financial stability / remove a significant amount of financial instability.

To find the entry value of 'C%' for a given total repayment period please visit Waghorn's Equations

Currently the title will be 'A tract on Financial Stability' or the short version will omit this and will be called 'A Short Tract on Financial Stability'.

Sections #2 and #3 of the book are covered quite well in outline on www.fin24.com in the later essays. There is a guide to those essays here.

No comments:

Post a Comment

Please type your comment here

Note: Only a member of this blog may post a comment.